This post is an accompaniment to the article I wrote about the similarities and differences of CFDs vs Spread betting. As there was quite a lot covered in that post already, I am adding this page to demonstrate how and why various charges are applied to your CFD positions in a bit more depth. It will also let you have a play around with a calculator I’ve made to replicate major providers ‘adjustments’ (as they like to call them), so you can see the impact of the different settings.

CFDs are confusing, just get on a helpdesk chat to one of the big providers and ask a few questions about charge calculations in their own documentation and you’ll be not at all surprised that they disappear off for a long while before coming back with a suggested answer.

The charges applied can also vary depending on which product group you are dealing with, whether you are long or short (have bought or sold), the specific share or instrument within that group, if its pricing is based off the cash (or ‘spot’) price or that of a future or forward contract, whether you declared yourself as pro or retail, if you want to be stopped out of positions at a price level that is guaranteed etc. etc.

Breakdown of CFD Share Overnight Examples

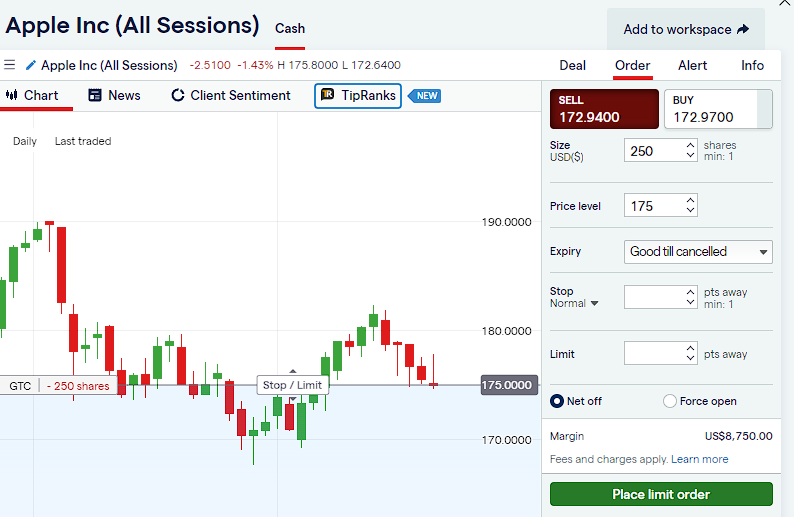

So to begin with, let’s suppose for the sake of this example you are a UK resident and you have funded your account in pound sterling accordingly. As the FTSE has been a bit of a dead horse for a decade or two you fancy some exposure to individual stocks traded over the pond. Let’s look at IG, one of the major CFD providers in the UK and aboard and see how they handle overnight charges.

As I write this it’s late October 2023 (IG have just cut 10% of their workforce). Searching the documentation regarding CFD charges from IG brings up some PDFs of customer agreements from 2020 referring to the outdated US LIBOR and some on-site examples of the same walkthrough but updated to use SOFR (US LIBOR’s replacement). The SOFR rate is still being quoted around 1.25% but bear in mind SOFR today is actually 5.35% after the rampant inflation and rate rises by central banks since.

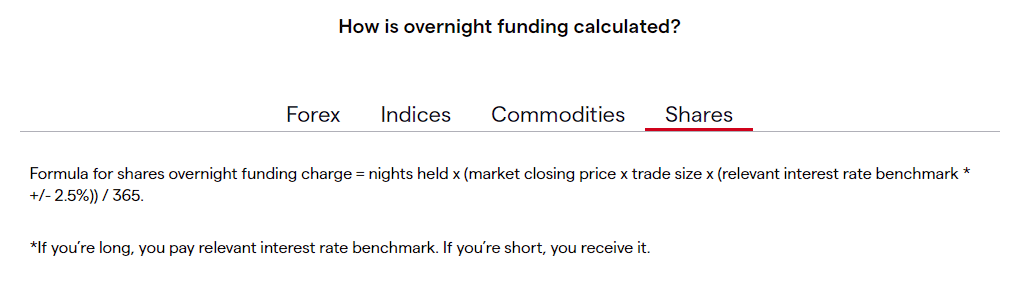

The 2.5% you see in the Overnight funding calculation is their extra admin fee, which is added on if you are being charged interest, which happens on long (open bought) positions and is discounted from the interest you receive which happens on short (open sold) positions. Note their example calculations use a 360 day convention to account for the number of days in a year but their explanation below says they use 365 days:

Elsewhere on different IG country specific sites, there is some more clarity on when 360 days is used by them and when 365 is used.

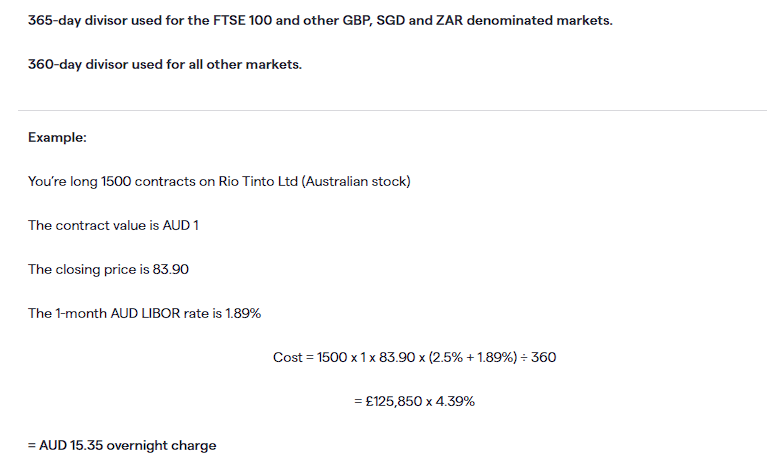

In the screenshot above it is worth noting they refer to the SONIA reference rate being used (rather than SOFR), which is GBP specific (Sterling Overnight Interest Average) but then oddly go on to give an example of an Australian-dollar denominated share below. That would have originally used AUD LIBOR as is shown in their worked example but it was actually discontinued back in 2013 and these days AONIA (Australian Overnight Index Average) has replaced it.

We get more clarity on the 360/365 day choices as shown in bold text above the AUD share example:

To 360 or not to 360 That is the Question

So why is there this difference anyway? Generally speaking the use of 360 days versus 365 days in financial and accounting calculations is rooted in tradition, simplicity, and specific conventions associated with certain financial instruments. Here’s a breakdown of why each is used:

360-Day Year (Banker’s Year):

- Simplicity: Using a 360-day year (with 30 days per month) simplifies interest calculations, especially before the advent of computers. If every month is assumed to have 30 days, then calculations can be done more easily in one’s head or on paper.

- Conventions: Certain financial instruments, such as some bonds and commercial loans, use a 30/360 convention. This means they assume each month has 30 days and a year has 360 days for the purpose of interest calculations.

- Types of 30/360 Conventions: There are variations, such as the “30E/360” (or Eurobond basis) where all months are assumed to have 30 days, and the “30/360” (or US Bond basis) where some exceptions are made for months that don’t have 30 days.

365-Day Year:

- Accuracy: A 365-day year reflects the actual number of days in a common year. This provides a more accurate representation for interest accrual over a real-world year.

- Daily Compounding: For financial products that compound interest daily, such as many savings accounts, a 365-day basis is often used.

- Leap Years: Some conventions using a 365-day year might adjust for leap years by using 366 days in the calculation for that particular year.

Other Considerations:

- Actual/Actual: Another convention is the “actual/actual” (or ISMA basis), which takes into account the actual number of days in a month and whether it’s a leap year. It’s used for some government bonds.

- Regulatory or Contractual Requirements: In some cases, the choice between 360 and 365 might be dictated by regulatory guidelines or specific contractual terms.

So considering the GBP denominated products use SONIA as their reference rate and US markets SOFR, are these conventionally 365 and 360 days financial instruments respectively? Yes.

SONIA (Sterling Overnight Index Average)

SONIA is a benchmark interest rate for British pounds (GBP) that reflects the average of the interest rates that banks pay to borrow sterling overnight from other financial institutions. The SONIA rate typically uses the “Actual/365” day count convention. This means that the actual number of days in the period is divided by 365 (regardless of whether it’s a leap year). This was the case with the old GBP LIBOR rate too which also used 365 days. Others that use the 365 convention are the Australian Overnight Index Average (AONIA), Johannesburg Interbank Average Rate (JIBAR), Singapore Overnight Rate Average (SORA), the Tokyo Overnight Average Rate (TONAR) and Hong Kong Dollar Overnight Index Average (HONIA).

SOFR (Secured Overnight Financing Rate)

SOFR is a benchmark interest rate for U.S. dollars (USD) that reflects the cost of borrowing cash overnight collateralized by Treasury securities. SOFR typically uses the “Actual/360” day count convention, which means that the actual number of days in the period is divided by 360. The old US LIBOR also used the 360 day convention. Others using 360 include the Euro Interbank Offered Rate (EURIBOR) and the Euro Short-Term Rate (€STR) which replaced EONIA,

In essence, the choice between 360 and 365 days is based on a combination of historical conventions, the specific nature of financial instruments, and the desire for calculation simplicity versus accuracy. When dealing with financial products or accounting tasks, it’s crucial to understand and use the appropriate day-count convention.

Back to the IG Charges Breakdown

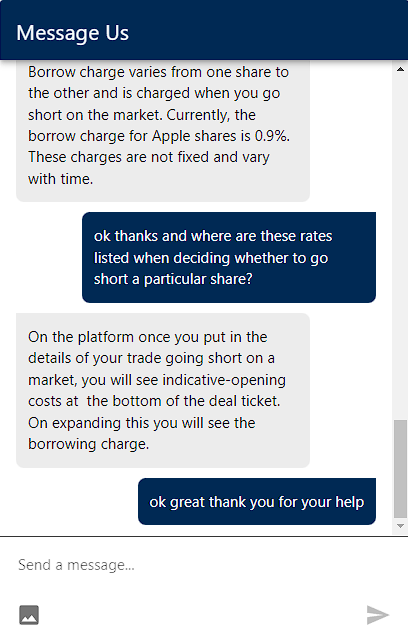

There are some things to note for USD share CFDs with IG. They charge a minimum commission of US$15 per side i.e. charged once to buy and again to sell (more if you do it by phone) and the “Borrow” charge is unique to the stock and its volatility at the time. Some brokers may keep this fixed for all stocks but I enquired with IG and they said theirs is variable, currently up at 0.9% up from the 0.6% in their original example for Apple shares on the day I asked:

Now looking for this ‘indicative-opening costs’ section proved tricky, in their desktop platform it didn’t seem visible, only a ‘learn more’ link to the sorts of examples we have discussed was visible on the order ticket as seen below:

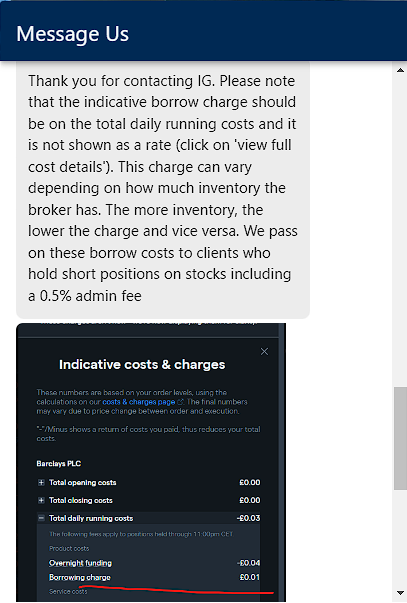

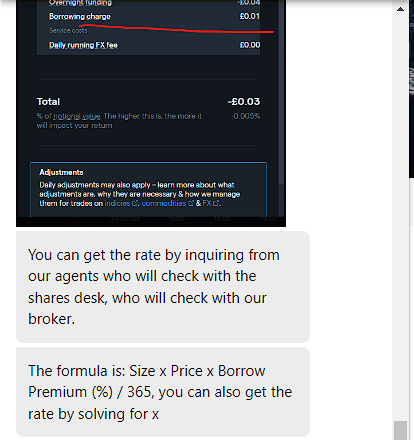

So I got back on the their help chat the next day and asked again. They said this time that the charge is not actually shown as a rate and supplied an example for Barclays PLC shares, although I don’t think this is the US listed Barclays ADR, it seems more like the UK-listed version and likely references the SONIA rate (replaced GBP LIBOR). However, they did say they still add a 0.5% ‘admin fee’ into the borrow charge whereas previously in their worked example from the pdf a 0.5% admin charge was only mentioned on the currency conversion rate. Other documentation found around IG since does say a 0.5% admin fee is included in the borrow rate which concurs with the chat response below. You can see they also say they used the 365 day convention which would imply this is indeed a GBP priced share using SONIA:

FX Conversion Costs

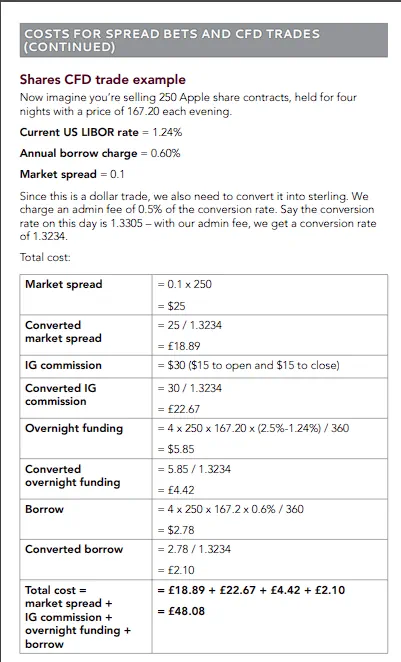

Referring to the short Apple stock example from the pdf shown near the start of this article let’s look at the currency conversion rate and admin fee costs we get charged. Attempting to add the 0.5% admin fee to their given 1.3305 conversion rate would result in 1.3238 not the 1.3234 they show. The only way to get 1.3234 in their example is to use a 1.33005 start rate, not 1.3305 – so it looks like a typo in their example. This equates to them charging you 66.5 pips extra conversion cost on that day compared to where actual market was trading. It’s not horrendous, most clearing firms I have worked with for futures would do my conversions for a fixed 15 pip charge, most high street banks would tend to charge you around 300 pips.

So let’s plug the calculated example numbers into a calculator form which you can then edit, we follow them in using the 360 day convention for this USD denominated trade for the reasons we covered.

CFD Charges Calculator (GBP account trading USD shares)

Results

Total Cost:

You’ll notice their total result is £48.08 total but ours is £48.09, even after we adjusted for their starting fx rate typo. After examining their calculations I found this is because their “Borrow” calculation, 4 x 250 x 167.2 x 0.6% divided by 360 = 2.7866 which would round up to $2.79 not the $2.78 they go with. The ‘Converted borrow’ would then be $2.79/1.3234 = 2.1082 which would round to £2.11 not the £2.10 they use and so adds an extra penny to the final outcome.

You can edit all the fields on the calculator above except the Adjusted Conversion Rate one which automatically adds 0.5% charge to the GBP/USD market fx rate field above it.

Summary

So I hope this has given some insight into the various costs associated with holding overnight positions in CFDs, particularly for shares in different currencies to your account. I will endeavour to put together other articles on different CFD products and how they are handled for for their own specific ‘adjustments’.

Leave a Reply