Introduction

In recent years, the Bank of England (BoE) has undertaken a significant reduction of its balance sheet, transitioning from the era of quantitative easing (QE) to quantitative tightening (QT). This shift, marked by the active sale of government bonds, has led to a notable liquidity crunch in some sectors of the money markets. As investors and analysts observe these developments, questions arise about the sustainability of this strategy and its broader implications for financial stability.

Background on BoE’s Balance Sheet Reduction

During the years of QE, the BoE’s balance sheet expanded to nearly £1 trillion. This expansion was driven by the central bank creating money to purchase government bonds, thereby injecting liquidity into the market. This liquidity helped stabilize and stimulate the economy during periods of downturn. However, over the past two years, the BoE has reduced its holdings to approximately £760 billion. Unlike other central banks, which primarily allow bonds to mature naturally, the BoE has proactively sold these assets back to investors, a move that has significant implications for market liquidity.

The Mechanics of Quantitative Tightening

Quantitative tightening involves two primary mechanisms: allowing bonds to mature without replacement and actively selling bonds back into the market. This process effectively destroys the money received from these transactions, reducing the overall liquidity that had previously been abundant. The intended outcome is a gradual normalization of the balance sheet. However, this strategy can lead to unforeseen consequences, particularly in short-term lending markets.

Money Markets and Liquidity: Explained

Money markets are where short-term borrowing and lending of funds (typically less than one year) take place. They are crucial for maintaining liquidity in the financial system, allowing institutions to manage their short-term cash needs effectively. When a central bank like the BoE buys bonds, it increases liquidity by injecting money into these markets. Conversely, selling bonds pulls money out, reducing liquidity. For the average person, this process affects loan availability and interest rates, impacting everything from mortgage rates to the cost of borrowing for small businesses.

Understanding the Gilt Market and Repo Facilities

The gilt market is where U.K. government bonds are bought and sold. These bonds are essentially loans investors give to the government, which pays back with interest. The repo (repurchase agreement) market is a segment of the money market where participants borrow cash short-term by selling securities like gilts and agreeing to repurchase them later at a slightly higher price. The difference in price implies an interest rate, known as the repo rate. High repo rates indicate that cash is scarce, and borrowing it is expensive.

Current Market Reactions and Challenges

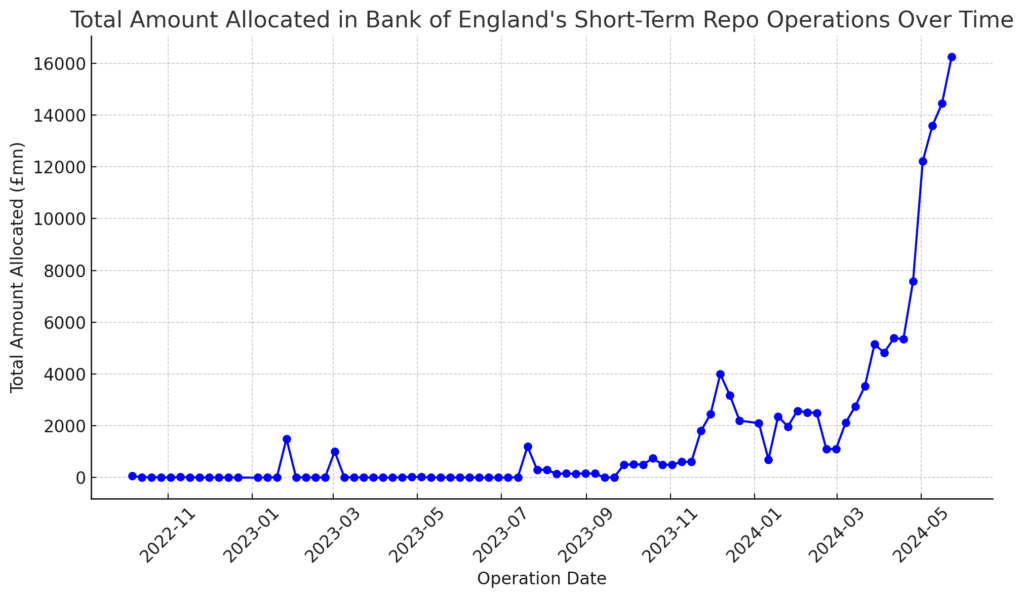

The reduction in liquidity has significantly impacted the short-term lending markets. Investors have increasingly turned to the BoE’s short-term repo facility, established in 2022, to obtain cash against government bonds as collateral. Last week, investors borrowed £16 billion from this facility, and today 17.186 billion pounds up from only £5 billion at the beginning of last month, indicating a growing scarcity of cash and rising repo rates. This surge points to increasing concerns among market participants about the availability of liquid funds.

BoE Governor Andrew Bailey has acknowledged the increased usage of the repo facility, describing it as “encouraging” and predicting a “significant increase” in its utilization. Bailey’s estimate for the steady state of the balance sheet ranges between £345 billion and £490 billion, but some analysts believe the actual figure necessary for smooth market functioning could be higher.

Potential Policy Adjustments

Considering the recent market dynamics, there is speculation that the BoE may slow down its QT efforts when it reviews its policy in September. Mark Capleton, a strategist at Bank of America, believes that the BoE might halt active gilt sales from September, partly due to a substantial volume of gilts maturing next year. This potential pause would provide the market with some much-needed relief and stability.

Why Halting the Sale of Gilts Provides Relief

Pausing the sale of gilts can provide relief and stability by alleviating the pressure on liquidity. When gilts are not being sold off aggressively, there is less upward pressure on repo rates, and more cash remains available in the money markets. This stabilization is crucial for maintaining the smooth operation of the financial markets, impacting everything from bank lending practices to investment decisions.

Broader Implications for the Financial Market

The tightening of liquidity affects all facets of the financial market. Higher borrowing costs, reflected in rates like Sonia, can lead to tighter financial conditions. This makes it more expensive for banks to lend and for businesses and consumers to borrow, potentially slowing economic activity and impacting financial stability.

Conclusion

The Bank of England’s strategy of actively selling government bonds as part of its quantitative tightening measures has led to notable shifts in the money markets. As liquidity tightens and short-term lending dynamics evolve, the central bank faces critical decisions on the future pace of its balance sheet reduction. Market participants and analysts will closely watch these developments, recognizing the profound impact of central bank policies on financial stability and market functioning. Understanding these complex interactions is essential for navigating the evolving financial landscape, highlighting the interconnectedness of central bank actions, market liquidity, and economic stability – and perhaps more importantly your trading decisions.

Leave a Reply